Recently I was asked to write a full-length article for the Forbes website by one of their regular columnists, who I’ll call “Pat” to protect the guilty.

Pat had taken my Financial IQ Quiz and found it very insightful. So Pat asked me to answer ten questions in writing for publication in Pat’s column.

The questions indicated Pat knew full well that I have a contrarian take on Wall Street and that I’m an advocate for consumers and investors.

They included questions like…

- “What are some of the scams in the mutual fund industry?”

- “What’s the shocking truth about 401(k)s and IRAs?”

- “How can investors protect themselves?”

So I painstakingly answered Pat’s questions, supporting each statement with highly credible, unimpeachable sources including Morningstar, the Securities and Exchange Commission, Government Accounting Office and the Department of Labor.

As requested, I made no mention of Bank On Yourself or the asset it is based on (super-charged dividend-paying whole life insurance).

About two days later, Pat thanked me for sending the article, but declined to run it “because there’s just too much controversy” surrounding my work.

Pat even suggested I repurpose the content for my blog (a good case for “be careful what you wish for”…).

So below are Pat’s questions with my answers in full, which I think you’ll find very interesting. Some of these questions I’ve never addressed publicly before. (Check out question #5 about “what mutual funds do you recommend?”)

I really want to hear from you… AND I want you to read the answers I wrote, because it’s critical information you need to know to protect yourself and your hard-earned savings.

So just tell us in the “Speak Your Mind” box at the bottom of this post your thoughts on any or all of the following:

- Which answer or fact is the most surprising to you and why?

- Which answer or fact is the least surprising to you and why?

- What do you think is the real reason Pat got too scared to publish this article on Forbes? (Pat is a staunch Wall Streeter who typically interviews portfolio and fund managers)

Now Here are the Answers to the Questions I was Asked by Forbes That They Got Too Scared to Publish…

1. What are some of the scams in the mutual fund industry?

For starters, mutual fund companies and the financial media love to tout and compare the results of funds over the past year, or past three or five years. And people make decisions about what funds to buy based on those performance records.

But the fact of the matter is that the only way to reduce or eliminate luck as a factor in performance results is by looking at track records of at least 15 years. Even a ten-year track record isn’t long enough, according to the well-respected Hulbert Financial Digest.

The second thing to be wary of is putting much faith into the performance reported in a mutual fund prospectus.

Case in point:

The top-performing mutual fund for the decade ending November 20, 2009, enjoyed an 18% annual return. However, the typical investor in that fund didn’t come anywhere close to getting an 18% annual return. In fact, they actually lost an average of 11% per year – every year – for ten years, according to Morningstar, Inc.

Wondering how that’s possible? It’s because mutual funds are legally required to advertise only the results of “buy-and-hold” investors. So when a fund advertises returns for any given period – in this case, a decade – it assumes investors bought the fund on the first day of that period and held it until the last day of the period – no matter how wild the ride got. But that rarely happens in real life. In fact, on average, investors hold mutual funds for less than five years.

2. What’s a secret that the mutual fund industry hopes people don’t ever find out?

The fees in far too many mutual funds are horrific wealth-killers. The fund industry hopes we all continue to believe that a fee of .5% or 1% a year is pretty insignificant.

The problem is that, in the case of mutual funds and retirement accounts like 401(k)s and IRAs, the fees are tacked on, and fees that compound against you can be devastating.

An annual fee of just 1% per year – and many people pay at least that inside their retirement accounts – will devour 28% of your savings over the next 35 years, assuming your returns average 7% per year, according to the Department of Labor.

People also assume that if you buy an Index Fund, the fees are going to be quite low, because it’s simply tracking an index and not being actively managed.

But I did an exposé in which I found that a very popular, widely held S&P 500 Index Fund will consume almost 23% of your money in fees over 30 years. And another S&P 500 Index Fund will siphon off more than 37% of your money over 30 years! If you had $1 million invested in this fund, that’s over $370,000 lost to fees! Someone’s getting wealthy, but it’s not the poor investor in those funds!

3. What percentage of mutual funds underperform their benchmarks?

Fully 80% of all mutual funds, portfolio managers and investment advisory services underperform their respective benchmarks, according to The Hulbert Financial Digest. And that’s not only because of the fees they charge. The experts are humans, too, and they’re predictably irrational like the rest of us, buying and selling at the wrong times.

How to Add Predictability and Guarantees to Your Financial Plan

Find out how you can grow your nest-egg safely and predictably EVERY year – even when stocks and real estate tumble. The Bank On Yourself method has never had a losing year in more than 160 years! Request your FREE, no-obligation Analysis and find out how much your financial picture could improve.

REQUEST YOURFREE ANALYSIS!

4. If most actively managed mutual funds lag their benchmarks, why do they have the majority of investor assets?

As Mark Twain observed,

A lie can get half way around the world before the truth can even get its boots on.”

But with new money going into funds, that’s changing rapidly, as “passive investing is now the mainstream approach,” according to Morningstar (“Do Active Funds Have a Future?” by John Rekenthaler, August 6, 2014). 68% of net sales went into passive exchange-traded and mutual funds versus 32% that went into actively managed funds, during the previous 12 months.

5. What mutual funds do you recommend?

I’m an educator and consumer advocate, not a financial representative, so I don’t make any specific fund recommendations.

What I can do, however, is suggest a simple three-step approach to investing that our research reveals will give you the best chance of success and also ensure you enjoy a financially stress-free future:

Step 1: Before you invest, build safe and liquid cash reserves equal to at least two years of household expenses, for those inevitable emergencies and opportunities that will arise. This safety net will provide you with priceless financial peace of mind.

Step 2: When you’re ready to invest, only invest money you can afford to wait at least 20 years to recover, not your rainy-day money. Why 20 years? Because since 1929, we’ve had three market crashes where the Dow took between 16 and 25 years to return to pre-crash levels.

Step 3: Invest in low-cost indexed mutual funds that are benchmarked to the broad stock market. And verify that their fees are truly low – look for funds with annual operating expenses of .25% or less.

6. What is the shocking truth about 401(k)s?

Even Ted Benna, who’s considered the “father” of the 401(k), admits he created a monster that’s out of control. Trying to turn the average participant into a skilled investor simply doesn’t work. That’s why these plans are more aptly called “hope and pray” plans.

Congress passed the Pension Protection Act of 2006 with provisions for eligible workers to be automatically enrolled in 401(k) plans, unless they explicitly chose to opt out. So, who do you think the “Pension Protection Act” was designed to protect? If you’re thinking the employees, you’re wrong. It was designed to protect employers from liability. When they follow the law and automatically put your money into “default” investments – typically target-date funds – you have no recourse if you lose your shirt.

Do you assume your 401(k) plan administrator picks good funds? Think again. A study from the Center for Retirement Research at Boston College found that plan administrators choose mutual funds that lag comparable indexes. Their choices were just marginally better than a monkey throwing darts.

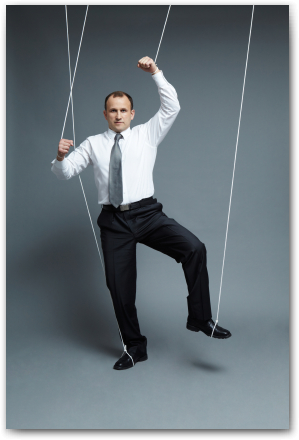

Another shocking secret about 401(k) plans that most people discover the hard way is that once you put your money in one of these plans, you lose control of it. These plans have more strings attached to them than a puppet.

You’re subject to restrictions on what you can and cannot invest in, how much you can borrow and how you must pay it back, how long you must wait before you can access your money, when you must access it, and how much you must withdraw (and pay taxes on) at that time. Penalties for running afoul of these restrictions can be very costly. Imagine needing permission to use your own money!

And then there’s the promise of deferring your taxes. Most people aren’t aware that if tax rates stay the same, and other factors are equal, you’ll end up paying the same amount in taxes whether you defer your current taxes or you pay them now and invest what’s left.

However, what direction do you think tax rates are going over the long term? If you think they’re going up – as most people I talk to believe – and you’re successful in growing your nest-egg, you’re only going to end up paying higher taxes on a bigger number!

7. What’s a dirty secret about IRAs?

They have most of the same strings attached to them as a 401(k) and the same downsides I just described.

And a lot of people assume IRA fees are negligible, but hold on to your wallet, because a Government Accounting Office (GAO) study in 2013 blew the roof off that myth.

Have you ever left a job and rolled over your 401(k) into an IRA managed by the same firm? Undercover investigators hired by the GAO found that seven of the 30 largest 401(k) providers incorrectly stated there were no fees to open or maintain an IRA. And half of the ten largest firms incorrectly advertised free IRA’s on their websites.

The study found that at one of the largest IRA providers, the annual advisory fee is 1.5% of assets with balances up to $500,000 – which means you can kiss goodbye 40-50% of your account value to fees over time.

8. How can investors protect themselves?

The Securities and Exchange Commission found that “investors have a weak grasp of elementary financial concepts, and lack critical knowledge of ways to avoid investment fraud.” Education is the key.

Question everything and invest time to increase your financial IQ. Start by taking our Financial IQ Quiz to discover and increase your financial IQ. It takes less than ten minutes to do, and you’ll get the correct answers and clear explanations immediately. Just by taking the Quiz, you’ll be much more savvy about personal finance and investing than most people.

9. How should people save and invest for retirement?

Start by knowing the difference between saving and investing. To save means to put money in a vehicle that is safe, protected from loss, and has guaranteed growth. To invest means to put money in a financial vehicle or asset that has a certain amount of risk and no guarantees of growth.

Investing money that you’re saving for things like college or retirement – which is money you really can’t afford to lose – is a sure-fire path to financial insecurity and sleepless nights.

Wall Street has brainwashed us into believing we have to risk our money in order to achieve any significant growth. My research and investigation into over 450 different saving and investing products, strategies and vehicles over the past 25 years proves otherwise.

How to Add Predictability and Guarantees to Your Financial Plan

Find out how you can grow your nest-egg safely and predictably EVERY year – even when stocks and real estate tumble. The Bank On Yourself method has never had a losing year in more than 160 years! Request your FREE, no-obligation Analysis and find out how much your financial picture could improve.

REQUEST YOURFREE ANALYSIS!

I was most surprised to learn that 80% of the financial advisers for Mutual funds could not beat the benchmark index or average for that type of investment and that the top rated fund over a ten year period actually lost money for most of it”s investors. If they just bought the index and did not manage the funds, they would do better than making their own picks. Why should anyone pay fees to money managers who cannot beat the market averages?

I am least surprised by the Fees that are being charged as I have heard of people typically paying 2-4% every year in fees for the money in their Retirement plans. If you pay these kinds of fees every year –regardless of market or fund performance– you will not have the retirement income that you are expecting.

Isn’t it amazing they ask you to answer their questions and when you do if they don’t like your answers you and your responses are dismissed!

Pamela; I am sure that those saving for their futures in mutual funds will be very surprised to read this article but also very grateful to finally understand why they haven’t been able to have success in getting to their financial goals. The fact that those that are so involved with mutual funds are confirming the long term negative impact of the fees and that most do not keep up with their index to begin with is a real problem. I hope this article will give people some good ideas that they can use to get on a proven track. Best Success and God Bless! Keep up the good work!

Hello Pamela; fantastic article! As a Canadian, we have some of the highest mutual fund fees in the world! The mutual fund industry is “self-regulated” in Canada and therefore can make up their own rules, fees, etc. We have RRSPs which is your 401K and our TFSA is your IRA. Same issues as you have because of them being Government controlled plans. Bank on Yourself saved our bacon after the last crash and we finally pulled all our money out of our RRSPs. We finally have peace in our lives when it comes to how to manage and grow our money. It’s the smartest thing we have ever done financially!

Thank you for your wisdom and knowledge!

If you do what the masses do, you will probably end up in the same place.

One day, a friend asked me, “Did you lose money in the crash of 2008?”

“Yeah. Who didn’t?”

“What are you doing differently today?”

(Silence)

That hit me hard. I hope it makes you think, too.

Wow! That is a strong and telling dialog!

A quote for “Pat” —

“What is a cynic? A man who knows the price of everything, and the value of nothing.” Oscar Wilde

Sometimes when the evidence is staring you square in the face, it’s impossible to see it because of the lenses we wear. I recommend Pat and the team at Forbes take off their glasses, and check out how much evidence they have to ignore to not publish Pamela’s article!

A quote for Pamela — “Kites rise highest against the wind, not with it.” Winston Churchill

It’s a shame this information isn’t more widely circulated. Even sophisticated investors lack the answers to the questions that you have addressed, Pamela. I met with a client yesterday and reviewed some of the funds he has in his retirement plan. He had no idea that the funds themselves had expenses that averaged over 1.5 %. Then on top of those are the fees he pays to his financial representatives. If people only knew. Thank you for the effort in opening people’s eyes as to what is really going on.

I think every high school and college student should have this as a mandatory read. I am in no way a financial guru but I do wish I had this article forced down my throat in my younger years. I now question what to do with all the money we have invested in our 401k…

Thank you Paula for attempting to get this information out to the general public… If course it’s controversial because of everyone knew the truth… Well, we all know what would happen.

You are correct and I couldn’t agree more wholeheartedly. I’ve thought this for years. Especially now that all my kids have been through the educational system which prepared them for nothing financial. Except for my son who became an Estate Lawyer, they are all pretty much clueless how to proceed or evaluate what goes on in the financial world. I, myself, was in my 40’s before my attention was drawn to finances…

I believe that the financial industry knows that people will not take the time to educate themselves on fees or the rules about investing. People are willing to listen to the experts ie the financial advisory who is human like ourselves; trusting them to make the best guess or better guess than we would. People also do not want to wait for a return. They want to see a big growth daily. Slow wins the race. The biggest surprise was the the rules that are in place to protectvthe money from you and not the financial representatives who can make millions off you with no risk. People need to educate themselves and look at all sides to make the best decisions. Keep up the good work.

The enticement of the Apple watch to write something worth while did in fact make me write something (apple watch). I thought the information was (apple watch) very informative and very helpful for me. You gave quite a few (apple watch) scary fact about fees that I am now worried about with my TSA plan (apple watch). Thank you for all the insight (apple watch) on these programs and please don’t stop what you are doing (apple watch)

Anyone who thinks our Government does us, the funders of it’s policies, a benefit that is not purposefully designed to pay back greater dividend to the Government, in the end, is naïve. IRA’s were designed with specific purpose- to give us an incentive to save, have a lot of our money go into funding the financial industry (under specific and self-serving Government control), and then to finally provide a future tax base for the Government. We all need to remember that a dollar is taxed multiple times just by passing it from one entity or business to another. No better way to move money, than to create a financial program that involves ALL of us, with specific rules about investing and then dissolving the investment at specific times and for “our” own good. Hmmm!

AND- here’s the kicker. If the Government helps provide you something like an IRA benefit and then needs those funds later, after they mismanage the economy- they’ll just rewrite the tax laws to take it from you and me.

We don’t have smart leaders and policy makers in our Government- we have the rich and powerful making laws and appropriating our tax monies into their own bottom lines and fortunes. Just look at the zero increases in Social Security cost of living benefits this year for those who have paid their tax bill as compared to the last self appropriated 33% raise for our Congressional Leaders, who receive a extra million dollars or so for a staff to do their jobs while they enjoy perfect health and life insurance benefits – all as prizes for being performers who would be fired from most any other position of responsibility based upon their despicable achievements. How many times did you actually pick someone who was not a member of that special rich club to vote for in a political election. Yep! It’s all about the “Club”, ’bout the” Club”!.

Take, for example, a policy of starting a war, spend our children’s money to pay for it and for political reasons and/or something like oil dominance that has nothing to do with humanity, kill off our youth without regard to homeland or family, tear up a country for those political reasons (like oil dominance and the pocket books of the oil companies and families) and then rebuild that country’s infrastructures at great profit to those who hold an interest in the rebuilders (who by-the-way don’t have to even compete for the contract).

We are pawns! If our economy crumbles or a new global currency occurs, we are all doomed who base our hopes on the System. Heck! Our Leaders and Financial Experts don’t even base their hopes on the system! Diversifying away from the “Amerika” Company Store makes a lot of sense to me!

Are there any Bank-on-Yourself Contracts involving globally invested and diversified Insurance Companies and products?

I’d have to say this is an accurate description of the current state of affairs. Educate yourself as best you can and make decisions accordingly. The so called financial “experts” are far too often pawns themselves for the CEO’s of big business who create and implement the narrative and systems that will benefit them while the masses think they’re doing the right thing because THAT strategy (their design) is what is being promoted in the media.

I want the truth but the problem is most people cannot or will not face up to the truth. Those that do are able to better armed to protect themselves when the next financial stock market collapse happens and it will happen and the question is does your financial plan work in good times as well as bad times? Thanks for speaking up Pamela.

Nice job, Pamela! Not surprising it was D.O.A. at Forbes as it would have a major negative impact on their advertising (and maybe subscription) revenue. In a prior life, I was home office underwriting manager for Life & Health Insurance for a major life insurance company. As such, I often attended meetings in which district sales managers introduced their agents to pre-tax retirement plans such as IRA’s. Often they would slide over the negatives and, in some cases, they omitted them entirely. When I asked them why they did this, a typical response would be, “If the agents knew the negatives, they wouldn’t sell the plans. And if their prospects knew the negatives, they wouldn’t buy them.”

Hi,

I am not suprised the article wasnt published. Who do you think pays for their advertising? One doesnt bite the hand that feeds it. My true suprise in reading this article was the fact that Pamela went ahead to in fact recommend low cost index funds for investors to buy. Even after removing the erosive effect of fees entirely, for the average investor with a buy and hold mentality, the stock market has been proven to be fraught with risk, short and long term. Better investments exist, and for the prudent investor BOY plans are an excellent vehicle to “park” investment funds pending when an excellent investment opportunity presents itself. Given the current economic climate, the stock market will suffer a significant drop in due course. Nobody knows when, but it will happen. As humans, we will inevitably react accordingly and sell at the wrong time,, locking in losses. We average Joes should get out and stay out of the stock market casino. Its always rigged for the casino to win.

The journey towards my financial education started four years ago. One thing is for certain, I can’t go back to the smaller way I use to think. I am determined to make a better future for my family. My worry is for my older sibling’s generation who are beginning to retire. They played by the rules, lived responsibly but will suffer the consequences of Wall Street and a government who do not have their best interests in mind.

Thank you, thank you for being a voice of truth and sobering reason. The main thing I took away from your experience with Forbes is that we do not have a free press. I will keep searching for news sources that dare state things as they are. Thank you for being one of them!

Pamela,

Some of the best things about your article were that it was short enough to read and easy enough to understand. Unfortunately it was all too easy to relate to. With every paragraph I could picture an event or situation that could have had a much better outcome with a little better plan-like BOY. We are so glad we found Bank on Yourself when we did and are working to get all of our children and grandchildren on board as well.

Here is a quote I found that sums up the frustration of, not only taxes, but 401Ks and IRAs:

Intaxication: Euphoria at getting a refund from the IRS, which lasts until you realize it was your money to start with. ~From a Washington Post word contest

Great article–joy kendall, MFT

I am most surprised that you recommend in your three step approach to investing step 2:

“Step 2: When you’re ready to invest, only invest money you can afford to wait at least 20 years to recover, not your rainy-day money. Why 20 years? Because since 1929, we’ve had three market crashes where the Dow took between 16 and 25 years to return to pre-crash levels.”

Since the last market melt down of 2007 or so, we have had one heck of a bull run in the markets, I don’t see how any particular interval makes more sense than another since we shot past the market DOW Jones high of 14000+.

Bullies take advantage of weaker people. From credit card companies to banks to sub-prime lenders and alleged financial representatives, we are all considered easy prey. It’s not surprising that, when controversial ideas challenge the status quo, they are stifled and swept under the carpet. After all, how many times have we ever really seen the bully defeated by the underdog, except for maybe in the movies.

This is some great info. Thank you!

What I fear is that so many people are complacent and seem to take the attitude of “That’s just the way things are,” and “Sure, they take a lot in fees, but what I do get to keep I wouldn’t have gotten otherwise.” I don’t think it’s just me that notices how the large majority of the population just takes whatever situation life deals them instead of taking the bull by the horns and educating themselves to be knowledgable and understand that they do control their own destiny. This applies whether they feel like they are trapped in a deadend job, a tough financial situation or whatever. There are so many options for the average Joe to take advantage of just by putting on their “big boy” pants and pulling up their boot straps.

If you blindly put your trust in some random “advisor” that has you sign a form acknowledging you have no guarantees then you deserve none. Would you let your kid get in a car with a stranger under the same circumstances? Then why do you put your future financial well being in that situation? You may as well just spend it all on lottery tickets and see what happens!

Turn off the TV. Pick up a book. Do some research. Protect yourself, your family and your legacy from being fleeced right out from underneath you.

Excellent info, Pamela! Bank on yourself is an idea whose has come. And the “the old tried and true” government sponsored retirement programs have raised the ire in people.

As for Forbes being too scared to publish your article, I offer this to illustrate my point: I refer to Galen who once dominated the field of medicine. He had been agreeing with the status quo of his day concerning the “tides” of the blood. They knew nothing about heart action. Another physician, an Englishman named Harvey, found by direct observation (animal vivisection) the actual function of the heart. When he made his announcement, immediately dead cats, rotten fruit and pieces of wine jugs were tossed in his direction. He raised quite a commotion in medical and social circles, until finally, in desperation one doctor made the historical statement that “I would rather err with Galen than be right with Harvey!”

Every so often rebels come along who are not satisfied with preponderance of opinion and who actually present real solutions. Where would medical science be today if Galen’s theories had obtained? Bank on Yourself came at the perfect time for me and my family and I only wish I had heard of it sooner. Keep up the good fight!

Wish I knew about this when I was younger.

Franklyn, me too. I’m 70. In “good enough” health, but never recovered from multiple hits (not just the market crash) in 2008. I guess the good Lord (or Lady) wants me workin’ till I die with my boots on! I doubt I can do much of anything with

BOY now.

I have been following “Bank On Yourself” for over eight years. I have never taken the plunge mainly due to the fact that my wife’s long term illness has eroded my retirement savings to a point that working two jobs is necessary. The point is, that in those eight years I have been following the system, I have never had a reason to doubt any claim or representation. In fact had I been able to invest just 30% of my retirement back when I first saw the program, I would not had to be working so much….or maybe not at all.

The taxes paid for early withdrawal of tax deferred savings and 401K plans, plus fees were devastating so my advice is to start B.O.Y. now rather than later.

The fact that Forbs and other major financial advisors have either requested or refused publish article’s on this program is all the proof you need.

” MONEY IS ONLY TANGIBLE IF YOU HAVE IT”

This is a very entertaining post that is also 100% accurate. You don’t see that combination too often today with all the financial pornography out there. I learned these lessons the hard way about 14 years ago and decided to go with Bank On Yourself. I have not regretted that move since.

Thank you, Pamela.

Alan Eckstrand

None of these scams surprise me. As a former Financial Advisor for a big bank (rhymes with Mells Dargo) I have seen the dark side of this industry first hand. I entered my new position bright eyed and bushy tailed thinking I would be helping people. However, one fact explains the reality. I and my fellow rookie advisors received two weeks of sales training and a few days of training on working with clients. Once in the field I experienced first hand how easy it is to manipulate numbers and how common the practice is. I was “coached” by my manager on what to say to a client to promote one product over another, numbers to reveal and numbers to leave out, and how to deliver the “facts” in just the right way. For example, I was coached to get my client into a fund that gave me a commission of $20,000 up front. With that kind of money on the line who’s best interest do you think I was looking after? Soon I realized that going after one client at a time was too slow and I could do the same thing by becoming the broker of record on a 401(k) plan for a business. With this strategy I could do the same thing I did with one client, but with 5 to 10 people at once! And the manipulation possible was even higher as we were not required to tell the employees about all of the hidden fees within the plan that would eat at their hard earned retirement funds. I read Bank On Yourself and a few other books and my eyes were open to what I was really doing to people. I realized that the best advice I could give my clients was the same advice Pamela gives in this article. Truly low cost index funds that track the broad market. At the same time I realized I can’t make much money with that advice so I left the industry for good. I was at the bottom of the food chain and the scams were real and common. I can only imagine that things get worse as you move up where more money, more jobs, and more power is at stake. I think that’s the real reason “Pat” wouldn’t publish Pamela’s article. Too much at risk for her and her constituents. After this experience I have zero dollars invested in the stock market. Zero! Thankfully I read Bank On Yourself, got myself a BOY Professional and I’ve never looked back. I’ve used my plan to invest in real estate, cover expenses during slow months, and as a secure holding place for my savings. Thanks for all you do Pamela! You, your book, and your team really changed my life.

I’m an insurance broker and skeptic in Las Vegas who found about “Bank On Yourself” from another insurance broker. I’ve read enough and seen enough You Tube videos to KNOW that “Bank On Yourself” is legitimate. I broke into the Life Insurance business with the battle cry of “Buy Term And Invest The Difference”. Unfortunately, approximately 87% of the clients who bought the Term Insurance didn’t invest the difference ! After their 20 year Term Insurance expired, they had nothing, nada, zilch !! I did the best for my clients that I knew at that time and we did help many people “Invest The Difference”. I wish I could turn back the clock 30 years and help EVERY ONE of those clients, but I can’t. BUT, I can help my 4 children and EVERY new client that I meet !!! Thanks Pamela for writing the 2 books, getting the word out through the media and your many hours of diligent research. – “Frank”

Very well written and very informative! I always wondered why I wasn’t comfortable with how companies handled their 401K plans. Thanks Pamela!

I’m a Main Street business owner. How does that relate to being part of a nudist community? (Not “colony,” as explained here: http://katiemccaskey.com/what-nudist-communities-can-teach-main-street/) Well, for starters both require a contrarian view. That’s exactly what drew me to Bank On Yourself. The points you make above are downright scary to most people (as scary, perhaps, as living without clothes or betting on Main Street). It’s refreshing to know not everyone follows the herd. Thanks for opening my eyes. I’m in year 2 of a BOY plan and pleased with the results.

Informative, succinct, and eye-opening article!

Most surprising: That mutual fund industries are only legally required to disclose the performance of buy-and-hold investors. That clearly shows the intent to deceive.

Least surprising: The fees — everybody’s in it for the money. That’s easy to understand.

Real reason Pat didn’t publish: She also wants/does the “apple watch,” get it? Her apple is the Wall Street advertisers, connections, endorsements, etc. WS peeps are enticed by the big apple (fees, commissions, performance bonuses), especially if they can get it with just a li’l fibbing. Who says it has to be moral? It just has to be legal.

If Gomer Pyle was able to write the title for your “refuse to publish” article; it would be-

“SURPRISE, SURPRISE , SURPRISE!”

Surprise-There are fees in those funds and they will eat at your returns!

Surprise- Average returns, buy and hold, net returns, smoke and mirrors! I’m with Will Rogers-“more concerned about the return of my money than the return on my money!”

Surprise- There is an alternative…educate yourself, know what’s available, explore your options, take that knowledge to the bank! Or better yet…”Bank on Yourself!”

where can a 78 year old man invest 100.000.? probably too old to buy life insurance.

Great article Pamela! Thanks for revealing the truth and not being afraid to telling it like it is. People definitely should read your book, The Bank On Yourself Revolution.

I only wish I had learned the truth 40 years ago. I am in my retirement and doing well. How much better if I had known then what I know now. Keep spreading the truth in spite of the “Pats” of the Wall Street world.

Three market crashes in less than 90 years requiring between 16 and 25 years to return to pre-crash levels. This is the most important fact to grasp. Couple that fact with compounding fees, and the number of years to recover your principle “investment” will be much longer? Past performance is not an indicator of future results, so if we do see a crash that takes even longer to return to pre-crash levels, think more than 25 years. Do you really have a few decades to let your principle “investment” recover?

Pamela, kudos to you for speaking what is typically not being said. i spent 17 years investing into the 401k plan only to see poor to negative returns, yet my adviser told me to just hang in there. I knew that education was my answer and hanging in there wasn’t. i found out that other investors have found other ways to build a solid financial future, and that i could do the same. So i pulled all money out of 401K- to put into a self directed IRA and also have been learning about the concept of bank on yourself using whole life insurance. I am convinced this is another avenue to help build wealth for future and actively pursuing an insurance plan to do that. But this concept is not embraced by all, even Dave Ramsey is apposed to it, saying that it is a poor investment, and recommends going to the stock market. I don’t get it! So keep telling your story, some of us are listening.

Kim

Even the comments are “pitchy”

It is not surprising to read these facts since we already know that the financial industry is first and foremost looking out for ITSELF and not the ‘investor’. I realized this some years back and decided to become a currency trader, and become the CEO of my own financial destiny rather than fork it over for someone else to manage, never really understanding what’s going on. Well, it took me 10 years to master the art of trading, and as soon as i can, i will be making use of Pamela’s information and opening up a 770 account. When ‘Pat’ at Forbes read this article, it must have hit a nerve…..perhaps she has a vested interest in keeping this truth silent. Or perhaps she’s up to her eyeballs invested in mutual funds that are under-performing for her, and the truth hurts too much. Or, someone else (her boss) read the article as well and found it ‘threatening’ to their special interests, etc etc. Do you think Wall Street wants these truths to become common knowledge?? Heck no.

I am a high school math teacher and I teach a personal finance class. I had my class take the financial IQ quiz last school year. When we cover retirement accounts I show videos that talk about the fees that are hidden in these accounts as well as articles from Pamela’s site that show the benefit of Bank On Yourself. I am proud to say that each year that I inform my students about this program I am able to generate interest and some students tell me that they will actively pursue this avenue when they get a steady income. My students hear only that the market is king from ads and sadly from our economics teacher. From talking with him, he knows about the principles but still believes that the market is the best way to grow your money. I like to think what would happen to Wall Street if people finally woke up and got out of the market. Also, glad to hear more ads on XM regarding Bank on Yourself, it’s what got me to check it out.

No matter how many times I see the data, I am still shocked at how poorly the investing public does compared to the published returns from mutual funds. My wife and I have Bank on Yourself policies and it is so reassuring to look at the policy values steadily increase every year and ignore the market volatility. Thank you for continuing to shine the light on Wall Street.

If you would have been willing to spend as much in advertising dollars as they would have lost by publishing the article they might have published it.

Many of the financial media have vested interests in promoting the next best product, solution or new strategy to their readers. It’s very sad that the ultimate consumer isn’t better educated so that they can make more informed decisions. It would be really if the financial media experts would spend at least some time in educating the public on the importance of building a strong risk protected financial foundation that provides efficiency, predictability, safety and lots of control. Keep up the common sense documented articles and solutions provided through the use of overfunded dividend paying whole life insurance offered by Mutual Life Insurance companies.

Mutual funds—ugh! There are more different family of funds then there are stocks listed on the NYSE. They even have different country funds. Funds from Korea, Japan, China, etc. but they basically have some things in common. There’re mainly dealing with stocks…just different stocks in one basket (fund). The other thing they have in common is it’s all still a crapshoot…house usually wins. Why do 75 to 80 percent of fund managers can’t beat the market? Heck the stocks they have in their funds are from the S&P, Dow Jones, NASDAQ, so figure the odds it takes to beat the market. Bottom line is…who cares about your money the most….YOU. So take your pick on where to save and invest and beware the pitfalls.

I removed all of my 401(K), IRA and pension money over the last 10 years. Asset protection is the #1 Rule. All the hidden marketing charges and rules guarantees just one thing: that i don’t have money of my money. I have commodity funds that are highly speculative but it’s something I can understand. Do I have all my money in commodities? No, only a portion I can afford to risk. The bulk of my money is in a “Safe Harbor” of bank money market funds. Based on my predictions, I feel there will be a crash in September to October 2015 time frame. I was lucky to predict the Black Monday Crash of 1987(I was out 2 weeks before that crash. I was fortunate to short the Bond Market in 1994 and paid for my private college degree(my 2nd one). I avoided the tech bubble & 911 crash of 2001. In 2008 I was out of the stock market but highly exposed to the real estate rental market which gave me a slight hit. I am fully aware september to october of 2015 will be a wild ride to hell. I write this on July 30, 2015. As a result, I am open to mutual stock paying dividend companies. I had opened one of these in 1986(when interest rates were high) as received a 10% compounded rate of return PLUS received stock when the company converted from a mutual company to a stock company. I have pulled out over $80,000 tax and penalty free in 2004 to start a successful commercial real estate practice-let me know what else can do all of that safely without sleepless nights? Pamela is dead on the money with her critique of the mutual fund industry-none of my wealthy friends have ever owned one.

I don’t have anything else to say but I’m returning the call! After reading this article and four years of getting these newsletters, I did the research on my retirement vehicles. I’m in my thirties and fell for the “retirement yr fund” company! I’m stepping out the box because I knew more than the reps handling my fund! Thank you!

Great, concise assessment of the “Retirement Fund” industry. All-in-all a pretty good synopsis of how wealth has been, and is being stolen from the middle-class/working-class American.

Thank you again for the information you provide. It is overwhelming trying to decide what to do with my retirement money. Their is so much information being sold out there and it can be a daunting task trying to decide what is the right thing to do. Your perspective is unique. I hope to learn more about it so I can make an educated decision on being secure and comfortable in retirement. Thank you once again.

Pamela

Thank you for your work! I was a member of a group utilizing many of the same concepts you speak of. My problem with that group was that they were primarily interested in helping a very privileged demographic and had a very right leaning bent. This always seemed egalitarian and counter productive to me.

Being based in the liberal Northeast, I truly believe that it isn’t which side of the political spectrum you are on what matters is if you are in the 1% or not. Criticizing one administration over another gains nothing in a retirement strategy that has been around since the early ’80s and one that is simply not working for most. By allowing companies to no longer fund a guaranteed Pension plan and instead put the entire responsibility on the Employee in exchange for a small percentage match IF they contribute (which sadly many do not) doesn’t work. What should have been the “3rd leg of a Retirement Plan” giving giving Employees some discretion over their money has become the 2nd leg of a 2 legged stool and we know how comfortable that is!

I tell people we may or may not agree politically but that really doesn’t matter. What matters is if you agree with me that the Government, and Wall Street, do not have your best interest at heart, period. If you are hoping for a comfortable retirement using your 401k/IRA/403b there is almost no way you will get there.

Your message through Bank on Yourself is so powerful (in my mind) because you speak to everyone, no matter what their current financial situation or political leanings. For the vast majority of us the system is very broken and people simply don’t see it. I speak with people every day who keep thinking their 401k will somehow magically grow to what they need by the 22% growth they expect to see in the market completely discounting the effect of fees and ultimately taxes.

By showing them a way to preserve capital and have tax-free growth it is truly an eyeopening experience for them.

Thank you for being a constant advocate of a more sensible approach.

Regards,

Scott

Comment:

I strongly believe in this concept and I would like to participate. Let me know if you have any suggestions. I am in the life insurance industry for 40 years would like to educate uninformed consumer about it.

I started a Bank On Yourself Policy last June. In that time I have been able to save more money than I thought was possible, provide security for my wife, and use the loan aspect to replace floors in my house. i love the concept so much my wife has just started her 1st Bank On Yourself Policy. How exciting is that!! And no fear of losing everything we work for over the next 5 years.

I sat in a meeting with my dad and his financial adviser just last week. Other than the obvious dislike for the Bank On Yourself Policy it was very interesting to listen to them explain everything from a bull market to why gold and silver is not the right purchase right now. During the meeting I felt like we were investing in a person and not the concept of building wealth. With Chris as my adviser our meetings are never about him and always about the concept and putting a game plan together to include the concept. After sitting through the meeting I feel more confident in my choice to start with a Bank On Yourself Policy as my saving vehicle especially reading the amount of posts that say, MY ONLY WISH IS THAT I WOULD HAVE STARTED EARLIER. Another difference I saw in the meeting is that my dad did not have access to his savings without penalties being taken out. So his investment is made up of risk, adviser fees, and no access without penalties. Sign me up!!

My parents love the concept and are as close as you can be to starting their own policies. Any advice on how to help them make the move. No risk only reward right??

Hi, Pamela, it’s me again. Question 6 is absolutely the one that anyone should read and heed. The ultimate goal of this whole principle is to grow your assest and avoid taxes (legally, of course). The biggest myth of 401’s,403’s, and IRA’s is to invest with before tax dollars. Couldn’t be any further from the truth! Your response to question6 is spot on and should be displayed in large, bold font. Full disclosure: I have several BOY policies which are serving me exactly as advertised, so per your instructions, none of your answers were surprising. The fact that you were not published is not surprising, either. I suspect this to be an attempt at “gotcha” that backfired.

Keep up the good fight,

Bill

Hey, to make a long story short, I need to invest my money in the service fees they are charging their clients!!!!!

Please STOP writing these articles.

I am glad that Forbes decided not to publish your work.

The more people who discover the secrets of the bank on yourself system, the more likely that the government will catch on and screw it up for all of us.

The tax free attributes of dividend paying whole life insurance is the one of the most attractive aspects of the bank on yourself concept.

I was recently told that I have a couple of molars that need to be removed and since I really like eating, and the hassle of dentures and all the stuff that goes with them gives me concern, I looked into getting implants.

It seems that implants are fairly costly and so I had to figure a way to pay for them.

I have 2 choices. Take the money out of my 401(k) and pay taxes on it or borrow the money from my whole life policy and pay no taxes. hmmm What shall I do?

A few comments seem to fit. “The problem ain’t what people think they know, it’s what people think they know that just ain’t so.” Will Rogers. OR “It’s just math.” OR “It’s not what you earn that counts, it’s what you keep!” Great expose’ Pamela,keep up the good work. By the way, as a criticism of mutual funds as well as qualified plans, you didn’t even mention the fact that they , with all their restrictions and shortcomings, are worthless when it comes to being able to “bank” through them. I guess you were being kind by only throwing them half way under the bus.

Kevin

I have been on the roller coaster of the stock market (401k’s) for years. Seeing my quarterly statements with negative numbers made me (puke) sick. Hearing an ad on XM radio, I purchased the B.O.Y book. It’s now 5 years . My first thoughts were I wish I knew of this financial vehicle sooner. I am now on the road to recovery. Looking forword to shifting the balance to my B.O.Y policy. There are no guarantees in life , Oh wait,maybe one. Better late than never.

I’ve researched the BOY concept for about a year now and it has really opened my eyes to many of the “tricks of the trade” in the financial services “game”. As a result, I’m in a difficult place. As a Financial Planner, I feel I was sold a bill of goods when I started in this business. Unfortunately, I’ve followed suit and have led a lot of clients down the mutual fund/ IRA road and even encouraged them to max out their 401Ks (to the point where the employer matches). I now find that I can no longer advise clients to invest in products I don’t believe in myself. As a result, I encourage more and more clients toward the BOY product. I know nothing is sure-fire 100% and will work everytime for everyone in every circumstance. Also, portfolios should still be well diversified and not everyone will qualify for the BOY plan. I spend a lot more time in account reviews, re-educating and helping clients see the big picture. For the public’s sake, this information needs to reach everyone. Education is truly the key. Thanks, Pam.

I was most surprised by answer #2. It’s mind bogling to realize how a small yearly fee can eat up such a big chunk of one’s portfolio. No wonder we have so many mutual funds! It’s a cash cow for portfolio and fund managers. I was least surprised by answer #6. Anytime the government comes up with a “new” anything, it’s usually bad news for the consumer. When the 401k’s were introduced some 35 years ago, it was a bailout for corporate America because it changed retirement from a defined benefit from the company to a defined contibution from the employee. Companies were off the hook for providing for their retirees and employees were on the hook to provide for their own retirement with the government always getting their share and more in the end. I believe in personal responsibility, but there should have been more options, like a before or after tax contribution to a super charged dividend-paying whole life insurance policy (employee choice for what fits their situation best). In fact, I was thinking, if the government would have started taking the Social Security Tax surplus back in the 1930’s when it first began, and bought every new born baby from that time forward, a dividend paying whole life insurance policy, and then gave it to them when they retired, we would all be rich today! The real reason Pat got cold feet and wouldn’t publish your article is easy. Follow the money! His bread is buttered by encouraging people to invest in the stock market and mutual funds (only with a little caution thrown in here and there), not discouraging them from doing it altogether because it’s a losing proposition.

I to heard about Bank On Yourself on the radio and have been following Bank On Yourself now for about a year. I’m not a full time investor just a normal working guy. I started because I wasn’t happy with what I have with my retirement roller coaster. I’m now ready to see if I qualify for the plan.

Thanks ,Pam.

The facts, data and references all point to the same thing: Main stream financial planning is filled with risk and poor results.

What I don’t understand is why normally rational, intelligent and logical people don’t change their behavior when presented with the facts outlined in the article. Clinging to the ideas presented by the main stream financial planning engine seems to be the only response some people can muster. I truly enjoy the energy and open-mindedness of the BOY community. Thanks

Thanks, my wife is getting ready to retire and has a 401k that she does not understand. I showed her your unprinted article and now she knows what to ask her financial adviser (church member & employee of financial institution).

YOU SAY THE RICH ARE STICKING IT TO THE NOT SO RICH ONCE AGAIN. SHOCKING. IF I HAD EVER HAD EMPLOYMENT LONG ENOUGH TO GET INTO ONE OF THESE PLANS I’D BE FIGHTING MAD.

The challenges are many. Between self serving politicians hat no doubt started with the best of intentions. They refuse to speak the truth. I asked a top politician in my state, Hawaii to address the issue of the state pensions n system being 5 billion underwater about 10 years ago, the answer I recieved was was shockingly moronic, that the pension was guaranteed by the state constitution. No one had seen the bankruptcy of major cities, where politicos had overpromised things they couldn’t possibly pay for.

Consumers refuse to investigate and invest in their own health, wealth and retirement processes. They will spend $200K for an education and never guarantee an income. They have relegated the intelligence of their most precious asset their children to bureaucracy that won’t let their minds expand to all they can be. The consumers answer to the frustration is a litigious mindset, that is how to get out of the rat race.

There are many problems with these types of investments. The fees are very detrimental to the investor. But front and center also is the impact that investing in these instruments can have if you choose the wrong funds at the wrong time and…at the wrong time in your life. Fund companies should not even offer these instruments to investors in their 50s. Why? If you were in your 50s and had invested in mutual funds in the late 1920s and you had stuck with those that did not fail, you would not have regained your principal until the early 1950s. A person within 20 years of retirement just cannot afford that kind of high risk. And “that risk” is now looming on our horizon. Depressions are cyclical events. The Federal Reserve Bank thinks that they can control such events. As we will soon see, they cannot. In fact, their machinations do nothing but exacerbate and enhance the horrible affects of these events.

I am ready to save my investments.

Great read! All too many people have lost sight of the difference between saving and investing. With a traditional bank being the typical default for savings and bank interests rates being ridiculously low, many people choose riskier investments in the hopes of making any money, often times without the cash reserves to support that strategy. Losses or lack of appreciable gains increase the desperation and one’s risk tolerance, often inappropriately. Many people are playing a game without knowing the rules and with their life savings on the line. Thank you for speaking your truth so that those who are willing to hear, hear. ?

Each point you made is valid and when researched is true. I don’t have a question that I would label “most shocking”. What is shocking is that someone entrenched like “Pat” would even ask the questions in the first place. They were probably looking for someone to shower them with platitudes about their industry but they obviously called upon the wrong person, you, to give them anything but the be truth. Your information needs to be shared over and over again.

Pamela, it’s obvious you put a lot of thought and validated research into these answers, and they are terrific. They provide the honest truth behind mutual funds, 401K’s, and IRA’s. The problem is that once people have their money in these vehicles, they are more afraid of the taxes and penalties to get out rather than the potential principle loss of that money. As my colleague Lester Himel wisely stated, “Consistency and predictability always outplay occasional brilliance.” Once people experience “occasional brilliance”, they wait for it to happen again and don’t even think about what they would do with it (and thus just watch their money go down again).

So, to answer your questions:

Which answer or fact is the most surprising to you and why? That 7 of the 30 largest 401(k) providers incorrectly stated there were no fees to open or maintain an IRA. I thought that would be illegal.

Which answer or fact is the least surprising to you and why? That there are many fees in 401K plans. Since the plans now must reveal them, it stares you in the face.

What do you think is the real reason Pat got too scared to publish this article on Forbes? Because the editor would fire him immediately for even thinking of publishing this!

Great job!

Debbie

The two parts of this I think are most important are explaining to people that 1) saving needs to come BEFORE investing and only after your real needs are met, and 2)challenging the idea that risk and reward are directly related….So often, with the usual bad advice they get (especially from “equity-loving certified financial planners and advisors”), it is the people who really need to save who have brainwashed into thinking that they can’t afford to save…every extra penny they get needs to go to some risky stock. I was a bit surprised when you recommended index funds at all. Although there are some lower cost ones, they still make a profit off your money. The easier, cheaper thing to do now is to go into the lists of stocks that make up an index or fund, and pick a few stocks to buy at a discount brokerage. This way, you also can eliminate ones you really don’t want to own. If you want to go for high growth, then maybe add a decent growth ETF or fund with someone always looking for new growth…..If you look at most index funds and mutual funds, you usually find the same stocks listed as their top holdings, again and again, so why pay someone to hold your money? Most people don’t need stock brokers anymore. And don’t forget to reinvest dividends! Any stock worth owning is worth reinvesting in until you really need the income.

Well worth reading! I like all your comments on IRA 401K’s Mutual Funds and stock market. I am currently working with one of your Bank on yourself agents and getting things settled.

Thanks for your help.

Jim

I think the only true reason they didn’t post this article is so that Suze and Daves heads didn’t explode on the spot. 🙂

Forbes is a joke. I read absolutely redicilous articles out of the magazine every month. As a truly educated advisor I often find myself in rage when I read articles about how awful life insurance is, or how it’s dumb for seniors to guarantee paychecks for life with annuities. I often laugh at the advisors who are featured. You see noting but elaborate ivory towers. Huge floor to window walls and redicilous designer brand office equipment. They fees you described Pam are exactly how that happens. All the general public needs to see are those images to justify everything you just wrote about the lucrative fees.

These advisor are the reason Forbes exists. They pay top dollar to be featured so they can keep a copy on their desk and say to clients “look at me, I am in Forbes.. If this article ever made it to print it would severely hurt their credibility.

Keep up what you and your team over at BOY are doing! Only a matter of time before this explodes!

Very good answers. Forbes won’t publish anything that contradicts the industry that buys all the advertisng for their magazine. Why don’t you use IUL for the Bank on Yourself strategies? The upside for accumulating cash value is much better than dividend paying whole life. Dividends after all are just a refund by the carrier for over charges of premium.

401k just another government run scam by the time the stock market crashes again you will not be able to recover what you have invested. I am tired of government trying to control us and what and where we give our hard earned money so they can throw it away. Thanks again for the knowledge and wisdom your awesome

It sounds like it is time to get off the diversification mutual fund horse and ride another horse all together different. I appreciate your knowledge that flies straight in the face of conventional advisers who tout a story similar to “The Emperor’s New Clothes”. I follow alternative medicine, why would I follow a main stream investing or savings protocol? Thank you for the wisdom you share!

Hi Pam,

This is a subject I am passionate about for many reasons. I will condense it to three reasons:

1). My father in law has an IRA like millions of Americans. Because of his required minimum distribution, he is now paying taxes at the HIGHEST rate in his 84 years! These qualified plans are a scam!

2). My wife and I are dentists and outgrew our office. We decided to build a new office and needed a down payment for the SBA loan. Where does the down payment come from? Our 401k? Our IRA? Our variable annuity? Are you kidding me? We would be devastated by taxes and penalties. Since we didn’t know about Bank on Yourself, we literally had to sell our paid for home to come up with the money. Ironically, we were doing what all the experts were telling us about saving money and yet we had NO ACCESS to it!

3). The above experience led me out of frustration to research a better way and we found a BoY Professional. I am now on a mission to reach out to my colleagues because no one is telling them about this wonderful plan. I even obtained my insurance license thinking I could find an even BETTER strategy. Bottom line, I am not married to this strategy, but if there is a better way to save money, I haven’t found it!!

Very helpful information – who knew fees were so detrimental to your wealth? No one pays attention to them. And learning that 80% of all mutual funds, portfolio managers and investment advisory services underperform their respective benchmarks is actually shocking. People need to start taking control of their own financial future and thoroughly understand all aspects of something before they get involved in it, rather than relying on “experts”. By the way, I would love to know what funds the dart throwing monkeys picked : )

So here we are analyzing the financial markets together. Great article. No doubt the original is laying shredded in a corporate waste can somewhere. As I peruse the investment papers I keep thinking of that laboratory full of white coated analysts with clipboards passing out darts to monkeys….and knowing full well that in the wild, monkeys don’t throw darts, they throw poo. So, perhaps the financial advisors are closer to our evolutionary ancestors than we think? (OK….I don’t believe in evolution; just taking some comic license here….). When there is money to be had you better make sure that the advisors you listen to have YOUR best interests at heart…NOT their timeshare in Dubai. The very term “Bank on YOURSELF” screams just that…..win, win…..and there are people out there that actually want to help me do just that?…Win?! Wow….Sign me up!

I have found it very odd over the years that “finance counselors” (and that term is very loosely used) always are quick to point out how much “gain” a certain investment makes after a severe downturn of market based instruments. An investment from 1995 – 2005 gains 31% ($100,000 now is valued at $131,000) yet the market crashes in 2006 and the investment loses 50%, The investment is now worth $61,000 and could take 30 years to regain to $122,000. A robust market yields 35% over the next 5 years which the finance counselor touts as “outstanding”. And has the audacity to tell you how great the market is doing because you’re making such a great return on your funds. Oh but the fund now is only valued at $82,350. So until the investment fund reaches $131,000, you haven’t made a dime because you haven’t reaped what you lost and until that happens, you’re still in a losing deal. Just like the example:

* Invest $100,000 this year and make a 100% gain = $200,000

* next year have a 50% loss = $100,000

* the following year have another 100% gain = $200,000

* the following year have another 50% loss = $100,000

100% gain

-50% loss

+100% gain

-50% loss

The counselor will tell you you’ve had a 25% gain over 4 years. Add the losses and gains (that what the counselor does) and you have 25%. But you started with $100K and at the end of 4 years you still have $100K. Where’s the gain? And that doesn’t account for the cost of living, so in essence, you lost more.

The most surprising fact to me is the compounding of fees and having these fees eat away at our growth. It was my understanding that fees would be a percentage of interest/dividend earned on an annual basis. If we were told the truth about the fees, fewer people would want to go this route.

The least surprising fact is that prime information is held back from us when you are seeking investment advice. Normally, the banker or agent makes a presentation of what they have to offer and try to sell you. In this case, “you don’t know” what “you don’t know”. The onus is on you to investigate. These people have a quota to fulfil and the more people in their portfolio the better awards/earnings, they receive.

Pat is scared to publish the article because it is going against the norm. She is probably being paid to represent these companies and could loose her job. We talk about “freedom of speech” and giving people alternatives, but, when the real facts and honesty is being presented, people get scared. Thank you for sharing your experiences and wisdom.

Pamela T. (Canadian)

I can’t believe they would not publish your answers. You are right on with everything.

All proponents of IRA,TSA and etc. should have to show and explain the rationale for their tax deferred “investments!

“You can’t handle the truth!” – famous line from “A Few Good Men” movie. Very pertinent as to why this is not in the mainstream financial world. All of the administrators of all of these mutual funds, IRA’s & 401(k)’s have successfully pulled the wool down over all of our eyes, making us think we need to be in these savings vehicles to provide for our retirement. Sure, the company match sounds good on the 401(k) plans, but after you factor in the fees paid out and the taxes paid out upon cash pulled out, it is a travesty as to what they are doing to us. Thank goodness for the BOY plans that you promote! My only regret is that I did not learn about this sooner and start earlier! Having to pull money out against my 401(k) for financial emergencies really did me in and I lost everything I had. Starting over with a BOY plan has me back on the right path and I look forward to a life of being my own bank and not having to rely on others for financing and to avoid being scammed by those in the investment world. We may not have the glitzy returns that some of these products occasionally get, but when you factor in the MUCH lower fees, dividends and NO taxes along with being able to borrow against your plan at any time, it is a complete NO brainer!!! In the BOY arena, you don’t lose money like you do in most investments — there is a great deal of comfort, knowing that, in this day and age. Thank you for the BOY products and for providing all of us a great alternative to the scammy investments out there!!!

Mutual funds are touted as the option of choice for most small investors. However, your answers to the questions, accurate as they may be, do not support the theory. Wall Street has no other reasonable options and therefore, publishing your answers leaves Pat at the DEAD END.

The mighty Forbes Magazine quakes at the thought of revealing the straightforward truth and squelches it to protect the titans of Wall Street from little ol’ Pamela Yellen. Thank you, Pamela, for fearlessly hurling stones at the financial Goliaths of the world.

Is there any chance that Pamela Yellen could rent some monkeys and have them throw darts at lists of stocks and mutual funds? She could call it the Monkey Fund, follow it for a few years, and use it to promote Bank on Yourself.

What I found most surprising: “…mutual funds are legally required to advertise only the results of ‘buy-and-hold’ investors.” I had no idea that such deceit was built into the process.

What I found least surprising: the devastating effects that fees have on 401K balances. I knew that because I’ve read Pamela’s books.

The real reason for Pat’s fears: he didn’t want to risk losing his job and becoming a pariah in his chosen field.

One last thought. “Pat thanked me for sending the Q&A, but declined to run it ‘because there’s just too much controversy’ surrounding my work.” Yes, and there’s a great deal of controversy among thieves concerning laws against thievery.

What surprised me most, Pam, was that 80% of mutual funds had negative overall return for their investors. It’s like having one oxygen/lung monitor but hooking it up to a horse, a cat, a German shepherd , and a thousand mice, then calculating the average oxygen consumption – and publishing and publicizing that average! The horse for sure will be above average, and the German shepherd might also be above average. But this average is so misleading, since none of the mice were anywhere near the average! And no wonder that the mice aren’t told the truth about this average rate they can expect to individually have. Meanwhile, the mice are sucking wind! – and not being told why!

Pam, thanks for your work on this – much appreciated!

Thank you, Pamela Yellen, for all that you do. Like most posters, I wish I had known about BOY thirty years ago. However, even if it existed 30 years ago, I would not have had enough personal financial education or savvy to recognize a good thing when I saw it! The most eye-opening fact I take from your article (and your book) is that most Americans are sitting ducks when it comes to investing our hard earned money. How can something so important be omitted from our educational system? Please, keep up the good work. P.S. I’ll be forwarding this blog to several people I’ve been wanting to introduce to BOY, but didn’t feel comfortable enough to do it.

I noticed that in the last 10 years my investment has stayed flat. But the fees keep coming and I get the same explanation that the fee is only 1 % of my account. TIME FOR A CHANGE !!!!!

“The devil is always in the details.” Thank you, for I never really thought about the difference between what it meant to save or invest. I now see and plan to “save” for my future and that of my child’s. Everything but Nothing surprises me…except the truth

The most surprising fact to me is that “68% of net sales went into passive exchange-traded and mutual funds versus 32% that went into actively managed funds, during the previous 12 months”. That is a real indictment on mutual fund “managers”, who make millions of dollars while computers do the managing!

For me, the least surprising fact is that 401(k)’s are a REALLY bad deal. Most people have been trained to believe that the 401(k) is the only way they are ever going to have any retirement savings. The truth is quite the opposite, as you have continually written about. The Bank On Yourself concept is proof that you don’t have to risk your wealth to grow your wealth!

Why wouldn’t Forbes print your replies?

When confronted with the truth, a healthy person examines their false position, compares it with the revealed truth, sees it as false, and adopts the truth as their new paradigm. A healthy person seeks, and desires to learn, as much truth as possible.

In this case with the Forbes columnist, the truth (as revealed in your carefully researched answers) would require him to examine his false beliefs and change his paradigm. This, he cannot do and remain true to the mission of his employer. You created cognitive dissonance in his mind, and the most expedient thing for him to do was to reject your article and hold to his false beliefs.

I like the concept that if you spend less than you take home, and save, you can build a great deal of wealth.

I also like real estate for building both income and appreciation in values so that one can win in two ways.

Pamela,

1. I’m most surprised by your Step 2 in question 5, sitting tight for 20 years. I got started investing with low cost mutual funds many years ago and did very well with a quarterly approach to the markets – until the mutual fund companies decided they didn’t like people doing that and put restrictions on the best funds.

2. I am least surprised on the performance of mutual funds and managed funds. No one cares more about your money than YOU. Many people fail to realize this and the market is built on convincing people to contribute their money to the cause of brokers and fund managers making THEIR money.

3. The article was not published because it speaks the TRUTH and FACTS about the financial industry.

Ted Benna, who’s considered the “father” of the 401(k), must be feeling pretty bad to see what he designed taken to such extremes that the common folk are on the losing end of the retirement needs.

I always say, ‘I don’t know, what I don’t know’. Thank you Pamela for creating this educational article. Now folks, stop the insanity. Do the right thing….. Rid yourself of these government plans. Declare your freedom!

I make all my own discussions, based on educating myself. I decide what I drive, what I wear, where I live, where I work, who I marry, and how many kids I have….. Why would I want anyone or any entity in charge of my finances? It seems that finances is a very important part of my life and by allowing others take my money and play with my money surely makes me feel like the picture in the article of the man on strings, like a puppet.

SHEESH!! Now I know of another way. Thank you Pamela!

Waiting 20 years to invest, as you suggest, just does not work for me and many of us at age 83. I think your article needed suggestions which would help all ages.

I’m from pitiful New Jersey. Moreover, I want to start a small airline company there. Furthermore, I want to get start-up capital from the Teachers’ Pension System rather than the Wall Street bankers. The terms would longer and a win-win for both parties. Be that as it may, my governor is Anti-Teachers’ Union. Therefore, I am not surprised that “Forbes” would not publish your answers. Beyond Wall Street bankers there are “no alternatives.” Also, I hate ‘Shark Tank!’

The gullibility of the American people, including me, never ceases to amaze me. Why? Why? Why are we so easily imposed upon by politicians and duped by marketers who SEEM to have our best interests at heart?

The sturdily planned Yellen Rescue Boat, aka The Bank On Yourself Revolution, appeared on my family’s watery horizon when the other sharp looking investment boats were invisibly taking on water. Your amazing and convincing alert is keeping us from sinking under the weight of invisible costs damage.

Thank you, thank you thank you for making sense of the contradictory advice that was washing over us, and for clearly lighting up the big picture. We are thankful to have your strong and knowledgeable BOY team pulling us into the Yellen.

After reading this I am vary depressed. I am 57 and have a 401k of 100,000 and a pension of 2,000 a month . I wish I would have known this sooner. I do have another job and was going to start another 401k but after reading this I don’t know what I can do at my age ? Saving two years expenses is impossible with all the debt we accumulated over the years. I have five daughters and have been helping them out when emergencies arise. I guess I’ll be working till I die.

It’s kind of strange feeling, but I found myself in not that different circumstances when my husband died when he was 53 and was 51, only I hadn’t had a paying job in almost 20 years, in Sept. 2008…

First, don’t be afraid to keep some cash as cash. I’d convert the 401k to a guaranteed interest option if there is on so you don’t lose it.

Then evaluate whether you have enough money/income to devote some of it to a BOY plan, if your health is good enough to get life insurance at a decent rate. In a few years (after you are 59 1/2), you will be able to draw on 401k money (after paying taxes) to help fund it if you have to.

I like to have sources of money in multiple places–it makes me feel safer than having it all with one insurance company, or one anything. I would never put all my savings in any one thing.