Inquiring minds often ask, “If the cost of term insurance increases substantially at each renewal due to the advancing age of the insured person, how can life insurance companies guarantee to keep the cost of whole life insurance policy premiums level?”

The answer has to do with the cash value feature of whole life insurance policies. This feature allows the insurance company to maintain a guaranteed level premium over the life of the policy. This is different from a term policy, whose premium increases at each renewal.

Whole Life Insurance Cash Value and Level Policy Premiums

Here’s how the level premium feature works:

For purposes of illustration, let’s assume that you are 25 years old, and you’ve decided that a high early cash value whole life insurance policy with a $1 million death benefit is exactly what you need for your family.

Because of your policy’s living benefits, you’ll be able to borrow against your policy to finance college for the children you expect to have. Later, when you’ve paid back the life insurance policy loans, you’ll be able to generate a significant retirement income from the cash value.

Your premium is guaranteed never to go up.

So, in our example, you pay your premium every month, and a portion of each month’s payment goes toward the cash value of your policy. Thirty years down the road, let’s assume your cash value has grown to $550,000. (Of course, your actual cash value will depend on the specific features of your particular policy.)

Whole life policies are designed so that at maturity—age 121 for most modern policies—the cash value will equal the policy’s death benefit, which, in this example, is $1,000,000.

So thirty years after you start your policy, when you’re 55, your life insurance policy will still have a $1,000,000 death benefit. If you were to die on your 55th birthday (perish the thought), the insurance company would pay your beneficiary $1,000,000.

But—and this is important: the life insurance company will keep the policy’s $550,000 cash value when they pay your beneficiary $1,000,000. If this seems unreasonable, consider what happens when you sell a home in which you’ve built up some equity. Do you receive both the value of the home and your equity when you sell? No. Your equity represents a portion of the value of your home.

It’s the same with whole life insurance: Your cash value represents a portion of the value of your policy

Because you have a cash value of $550,000 in this example, the insurance company needs to cover only $450,000.

Let’s keep going. Ten years later, your policy’s cash value has grown to, let’s say, $750,000 (again, your cash value will be based on your particular policy). Because you’re older, the cost of insuring your life is considerably higher. However, when you factor in your cash value, the policy is really only providing $250,000 worth of life insurance. The rest of the death benefit will come from the $750,000 cash value.

From the day you buy your whole life insurance policy until the day you pass away, the insurance company’s out-of-pocket risk goes down each year, because the cash value goes up! Thus, even in the face of increasing costs due to your ever-advancing age, your premium remains level. And that is guaranteed.

How Bank On Yourself-type high early cash value life insurance policies can provide a death benefit that increases over time

Here’s something else to like about the kind of high cash value life insurance policies used for the Bank On Yourself method …

In a Bank On Yourself-type high cash value policy, any dividends you receive and any paid-up additions you purchase can increase your death benefit as well as your cash value! So a policy that may start with a $1,000,000 death benefit can grow to $2,000,000—or more! And your cash value would then be guaranteed to equal that death benefit at maturity. This article explains how working with a Bank On Yourself Professional can give you a high early cash value whole life policy structured so you end up with more cash value and more death benefit.

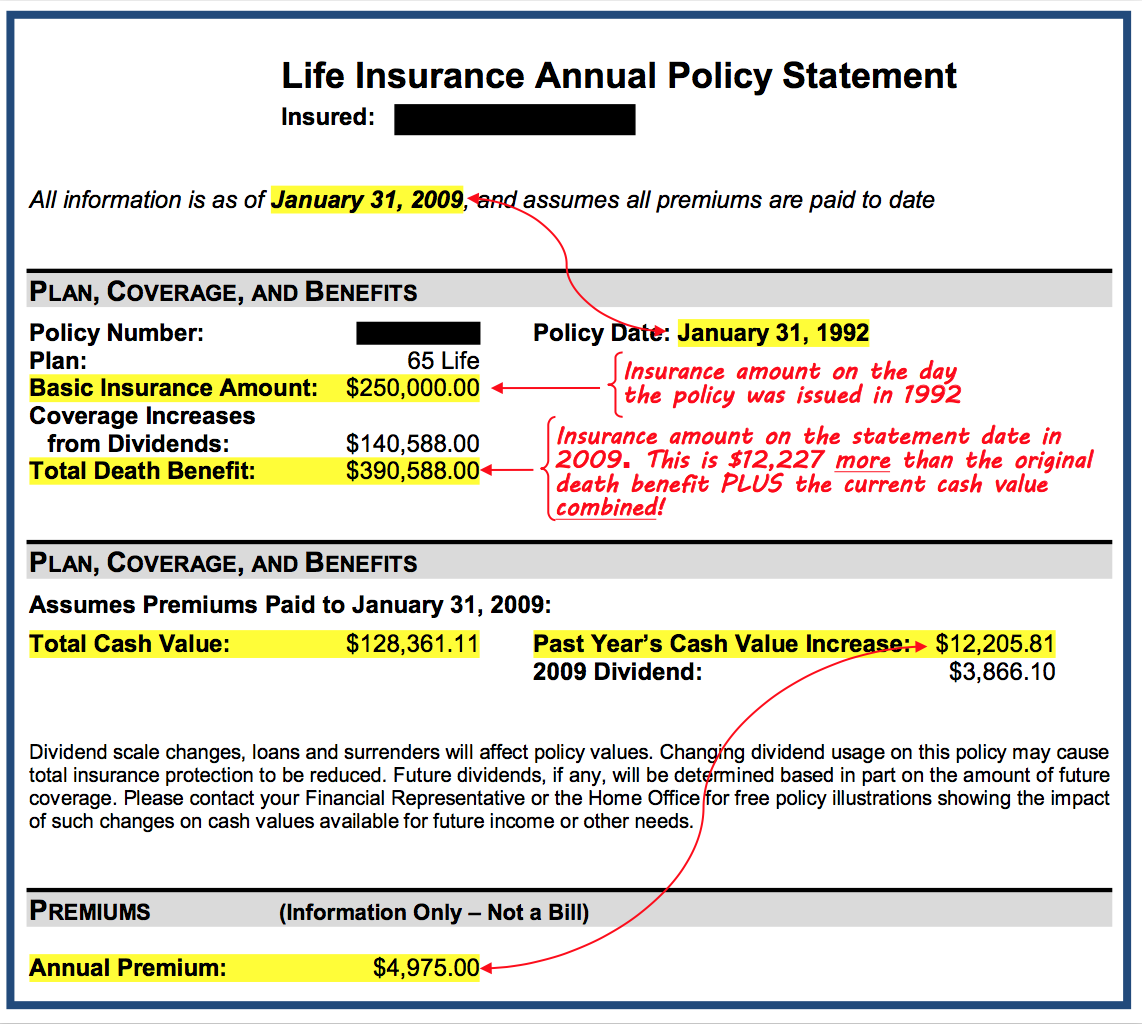

What happens to the cash value of a life insurance policy when you die? This Policy Statement reveals the surprising answer…

Take a look at this actual dividend-paying whole life insurance policy annual statement.

As you study this statement, do you see something almost unbelievable? The statement reveals what really happens to the cash value when the insured dies. It’s a factual answer to those who complain that when you die, the insurance company pays the death benefit but keeps your cash value.

If this policy owner had died on the date this statement was issued, her family would have received a check for $390,588.00, which is $12,227 more than the original $250,000.00 death benefit and the current $128,361.00 total cash value combined!

For more on the advantages of Bank On Yourself-style high early cash value whole life insurance plans, grab your copy of our free Safe Wealth-Building Special Report, 5 Simple Steps to Bypass Wall Street, Beat the Banks at Their Own Game and Take Control of Your Financial Future!

And to discover exactly how you can achieve your short-term and long-term financial goals in the shortest time possible—without taking any unnecessary risks—simply request a FREE Bank On Yourself Analysis and Personalized Solution. You’ll receive a referral to a Professional (a life insurance agent with advanced training on this high early cash value concept) who will prepare your Analysis and Solution for your review. There is no obligation!