Tax deferral is a con, and I’m going to prove it to you.

Actually, I’m going to let you prove it to yourself, with this 5-second experiment.

The conventional wisdom says, “Maximize your contributions to tax-deferred plans, like 401(k)s, IRAs and 403(b)s. Your money compounds without being reduced by taxes, and you’ll end up with more money during retirement.”

But is it really true?

The Society of Actuaries says that if the tax rates are the same, “It doesn’t make any difference whether [the taxes] are taken away from you at the beginning (tax-exempt) or at the end (tax-deferred). It’s the same fraction of your money that is left to you.”

But most people look at their savings and think it’s all theirs. You may have forgotten you’ll owe the IRS the taxes you deferred all those years – on every penny you’ve put in and every penny of growth.

If the tax rates miraculously manage to be lower during your retirement, you might come out ahead by deferring your taxes. But where do you think tax rates are headed long term? You must consider what tax rates might be during a retirement that could last 30+ years.

Most people realize taxes ultimately must go up due to the aging demographics of our country and our unsustainable national debt, which now exceeds the size of our entire economy. And if tax rates do go up, and you’re successful in growing your nest-egg, you’ll simply end up paying higher taxes on a bigger number.

Don’t take our word for it! You can prove it to yourself in seconds!

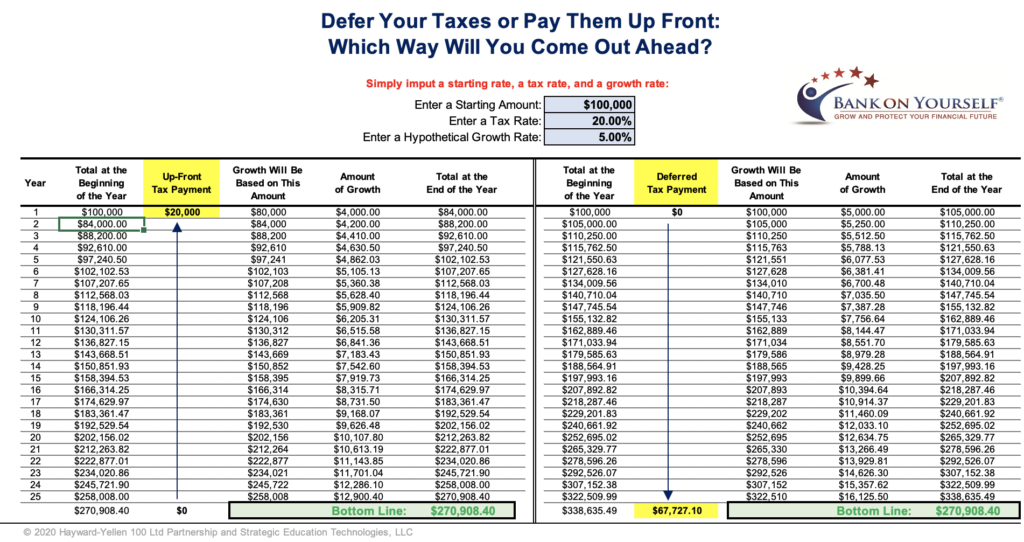

We’ve created a calculator that will let you see for yourself which way you’ll come out ahead. Just fill in any starting amount, any tax rate, and any growth rate:

Should You Defer Your Taxes or Pay Them Up Front? Click Here to Find Out Which Way You’ll Come Out Ahead.

You Just Proved that the Idea that You’ll Come Out Ahead by Deferring your Taxes is a Complete Con!

That’s why the Center for Retirement Research says it’s a very big deal when people realize they only have two-thirds of what they thought they had in their tax-deferred 401(k) or IRA retirement account.

And that statement was made before government spending fueled by the pandemic pushed the national debt to exceed the size of the entire U.S. economy… with no end in sight.

The reality is that in the highly likely event that tax rates go up during your retirement, you could end up paying many times more in taxes than you would have if you’d simply paid your taxes upfront, while you know what they are.

It’s bad enough that Americans have most of their retirement savings in government-controlled 401(k)s, IRAs, 403(b)s and similar plans, which have more strings attached to them than a puppet! These plans give you no guarantees of how much money you’ll have when you’re ready to take withdrawals… and no way of knowing how much of those withdrawals you’ll have to fork over to the IRS!

But There Are LEGAL Ways to Protect Yourself from These Inevitably Higher Tax Rates…

The Bank On Yourself safe wealth-building strategy helps protect you from higher taxes and expenses in at least 6 ways:

- Unlike with a 401(k) or IRA, you can access both your principal and gains tax free under current tax law – in fact, the income you take isn’t even reported to the IRS. Imagine knowing what your tax rate will be throughout retirement – ZERO!

- This strategy is not considered an investment, and the income you take isn’t subject to capital gains taxes.

- You can use it to reduce the taxes you may have to pay on your Social Security income. It’s become common for people to owe taxes on up to 85% of their Social Security benefits. However, the income you take from Bank On Yourself is not included when the IRS determines whether (or how much) of your Social Security check is taxed.

- It won’t increase your Medicare premiums. The income you take from conventional retirement plans – like 401(k)s and IRAs – can increase your Medicare premiums by as much as 350%! However, the income you take from Bank On Yourself won’t cause your premiums to increase.

- The Bank On Yourself safe wealth-building strategy relies on a high cash value, low-commission, dividend-paying whole life insurance policy, and comes with an increasing death benefit that passes to your loved ones income-tax free. This gives you priceless peace of mind.

- Many Bank On Yourself-type policies allow you to access a significant portion of your policy’s death benefit during your lifetime to pay for chronic or terminal illnesses or even to cover the cost of care in your own home if you prefer.

If You Want to Shield Yourself from Higher Taxes, It’s Critically Important You Take Action TODAY

Find out how you can shield yourself from taxes that can only go higher, grow your nest egg safely and predictably every single year, and enjoy liquidity, flexibility and control of your money.

Request a free, no-obligation Analysis here now. You’ll get a referral to one of only 200 financial representatives in the U.S. and Canada who have met the rigorous requirements to qualify to use the title of Bank On Yourself Professional. They can answer any questions you may have and show you the bottom-line guaranteed results you could get by adding the Bank On Yourself strategy to your financial plan.

They can also show you ways to find the money to fund your strategy, strategies for rolling over a 401(k) or IRA without owing penalties, and more.

Don’t volunteer to be a victim of the confiscatory tax rates that are coming. Click this button to get started:

REQUEST YOURFREE ANALYSIS!

Speak Your Mind