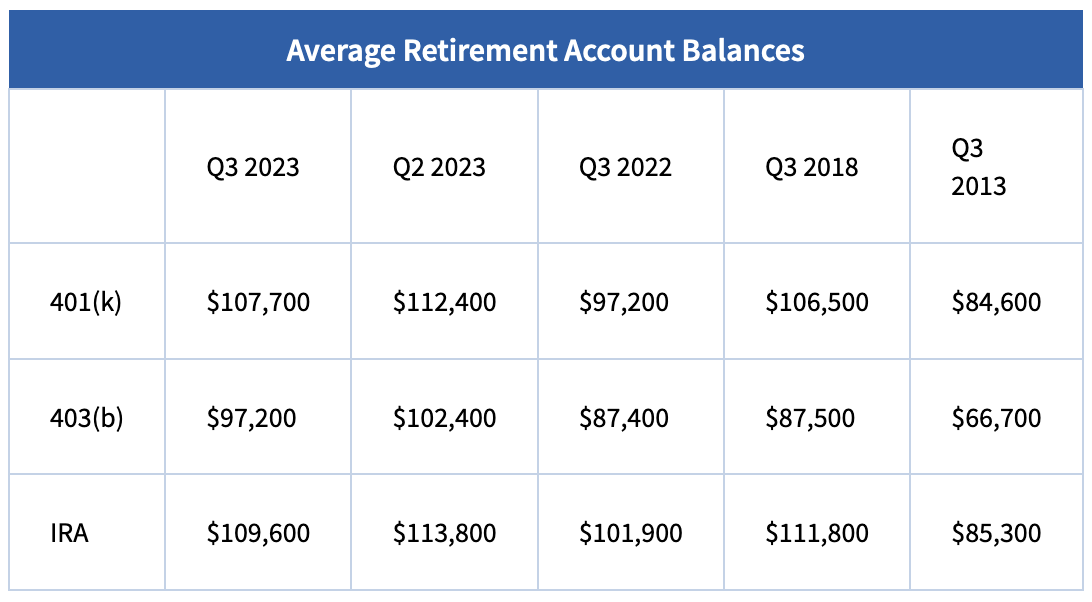

A recent article in the Wall Street Journal says it’s time to consider borrowing money from your 401(k). These loans have become more popular as more Americans get deeper into debt at high interest rates.

Most 401(k) plans offer participants the option to borrow from their plan. No credit check or collateral is required.

The IRS requires a mandatory repayment schedule of principal plus interest, currently 9.5% in many plans. That interest rate is lower than personal loans and significantly lower than the average credit card interest rate, making it appealing in today’s climate.

The article went on to explain the significant downsides of these loans. That got me thinking about how a 401(k) loan differs from a loan from your Bank On Yourself plan. So, let’s compare…

[Read more…] “Should You Treat Your 401(k) Like a Bank?”