Have you ever heard the old Wall Street adage, “In investing, the majority is always wrong”?

Have you ever told yourself you’re done with the stock market forever?! But then the market starts to rise. The Wall Street jocks tell you non-stop what you’re missing out on. Your friends talk about how much their investments are going up – and you jump back in because you can’t stand the pain of watching it rise day after day without you!

I heard a well-respected investment analyst interviewed about why he believed the stock market rally still had legs in spite of the fact that it had recently nearly doubled.

He said, “People who missed out on the rally will jump in and propel the market higher.” Really? Have you heard that old saying…

If you’re sitting at a poker table and you can’t figure out who the sucker is, it’s you?”

The investing world has a specific technical term for that kind of investing: dumb money. When the dumb money is piling into the market, you know it’s about to reach a top. And when the dumb money is fleeing the market, a bottom isn’t very far away. Dumb money, which is a heck of a lot of investors, misses the mark on both sides.

Students of history will tell you how rare it is for a market to continue rising after such an extraordinary rally – only a handful of bull markets in S&P 500 history have gained more than 100%. And right now, with the market up about 150% from the bottom, the air is even more rarefied.

The problem is that none of us knows when the market will top out… or how deep the crash that inevitably follows will be. History reveals that the faster and higher the market goes up, the steeper the fall.

The real estate market is getting pretty frothy, too. The Case-Shiller home price index was up 12.2% in May over a year ago – the biggest year-over-year jump since near the peak of the housing bubble in 2006.

Paper wealth versus real wealth

During the last bubble that peaked in 2007, few people anticipated that both their retirement accounts and their home equity would be decimated at the same time.

That’s when it became painfully clear that the balances of our investment and retirement account statements and the appraisals of our homes were nothing more than a bunch of eye-popping numbers on paper. Those numbers repeatedly sucker many of us into believing we have real wealth and financial security when we do not.

Last week, Wall Street journalist Brett Arends noted…

Mom and Pop investors have returned to the market and have been buy stocks since the beginning of the year. History says their timing is absolutely terrible.”

The last bubble burst just six years ago, and already many people have forgotten the pain of the Great Recession. According to the behavioral finance experts, part of the reason for this is that we humans have an amazing capacity to forget our losses and exaggerate our successes.

But the more important question is – what lasting lessons did you learn from the financial crisis?

Take this quick survey and share your biggest takeaway with us!

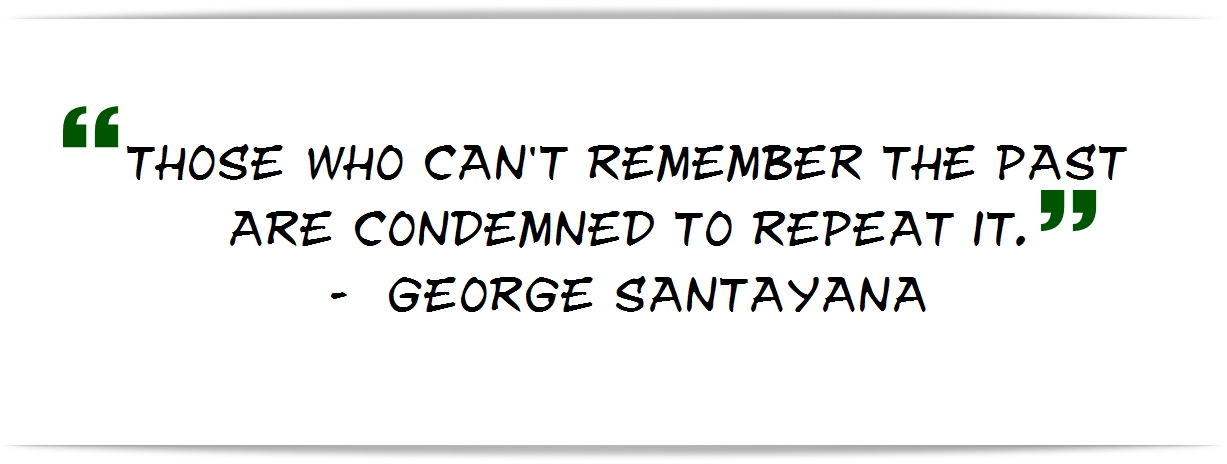

If you find yourself tempted to follow the “dumb money” into stocks, real estate and other volatile investments (and there’s no question that watching markets rise without you day after day can be very painful), I encourage you to keep in mind these words of George Santayana:

Take some time and reflect back on the lessons you’ve learned since 2000 before acting.

Then find out how much financial security and peace of mind you could have when you take the volatility and randomness of the market out of your financial plan. When you Bank On Yourself, your plan never goes backwards and both your principal and gains are locked in. That’s where the smart money is.

The typical investor lost 49% or more of their nest-eggs – TWICE – just since 2000. It could happen again in five or ten years… or even tomorrow. Is that a risk you really want to take again?